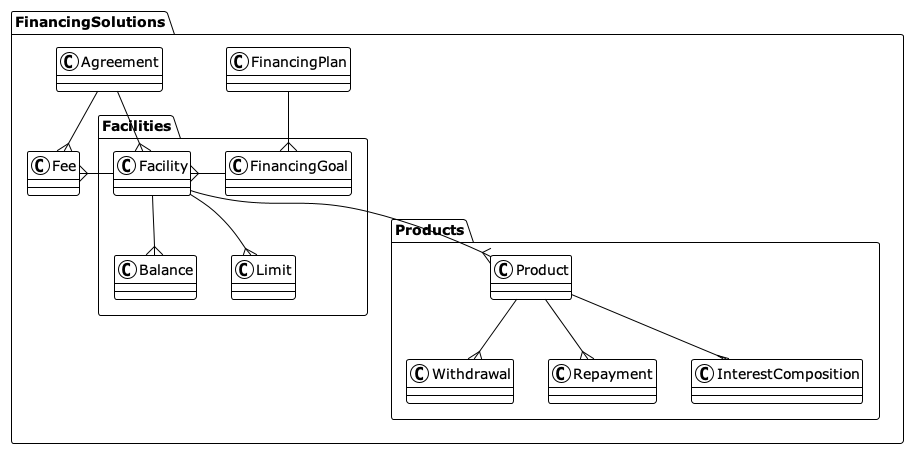

Financing Solutions

Overview

This document provides diagrams that illustrate relationships within the Financing Solutions domain. By understanding this model, you can visualize the complete data structure behind the Financing Solutions API, including how classes and attributes are organized and how their relationships are represented.

For a detailed description of each class and its attributes, refer to Financing Solutions API.

Financing solutions

The Financing Solutions domain represents the overall structure of a loan established between a lender and a borrower after the loan agreement is finalized. Loan structure refers to the constituent parts of the loan, such as the purpose, amount, type, interest rate, withdrawal, and repayment method.

This domain records all elements required to manage a loan, including agreements, facilities, and financial products.

- To learn how to read the diagram, see How to read these diagrams.

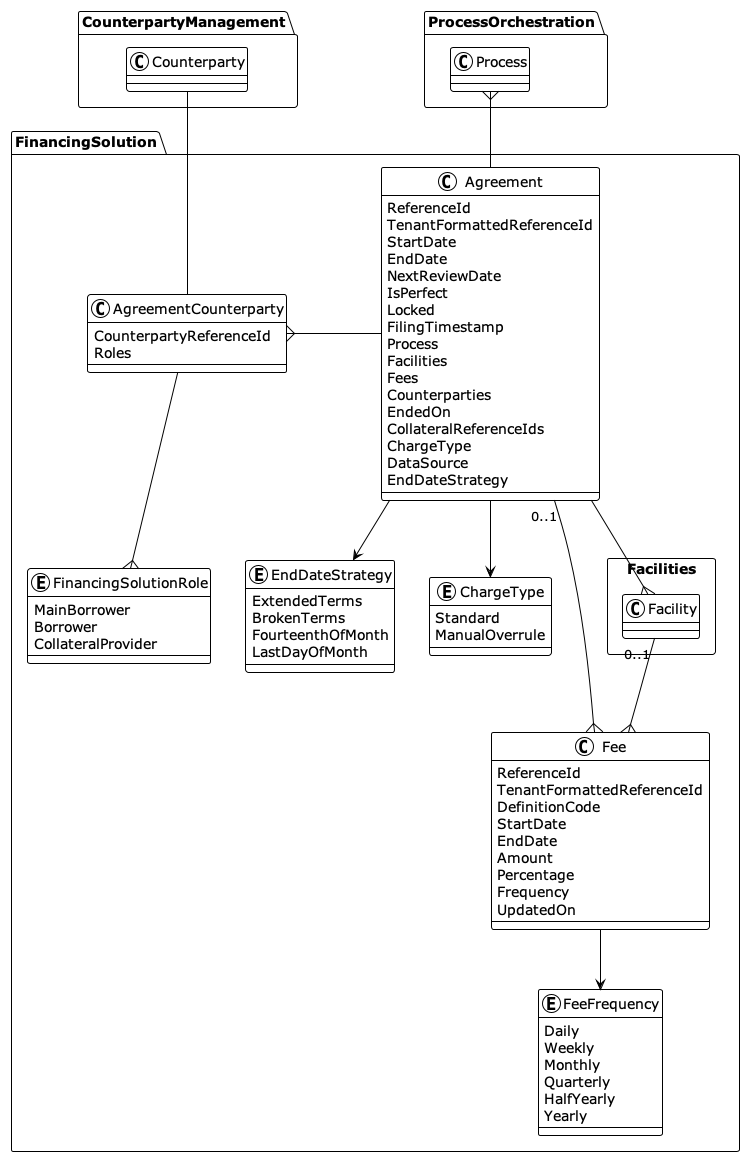

Agreements

- To view the diagram in full size, right-click and select Open Image in New Tab.

- To learn how to read the diagram, see How to read these diagrams.

An agreement serves as the legal foundation for the financing solution. It is a formal contract between the lender and borrower that defines the loan's terms and conditions. Each agreement may contain one or multiple facilities, depending on the complexity of the financing.

To retrieve agreement records, use one of the following APIs:

- Agreements Operational Query API to retrieve operational data.

- Agreements Master Query API to retrieve master data records.

Fees

A fee is a charge or cost associated with the loan that the borrower must pay in addition to the principal and interest.

To retrieve fee records, use one of the following APIs:

- Fees Query Operational Query API to retrieve operational data.

- Fees Query Master Query API to retrieve master data records.

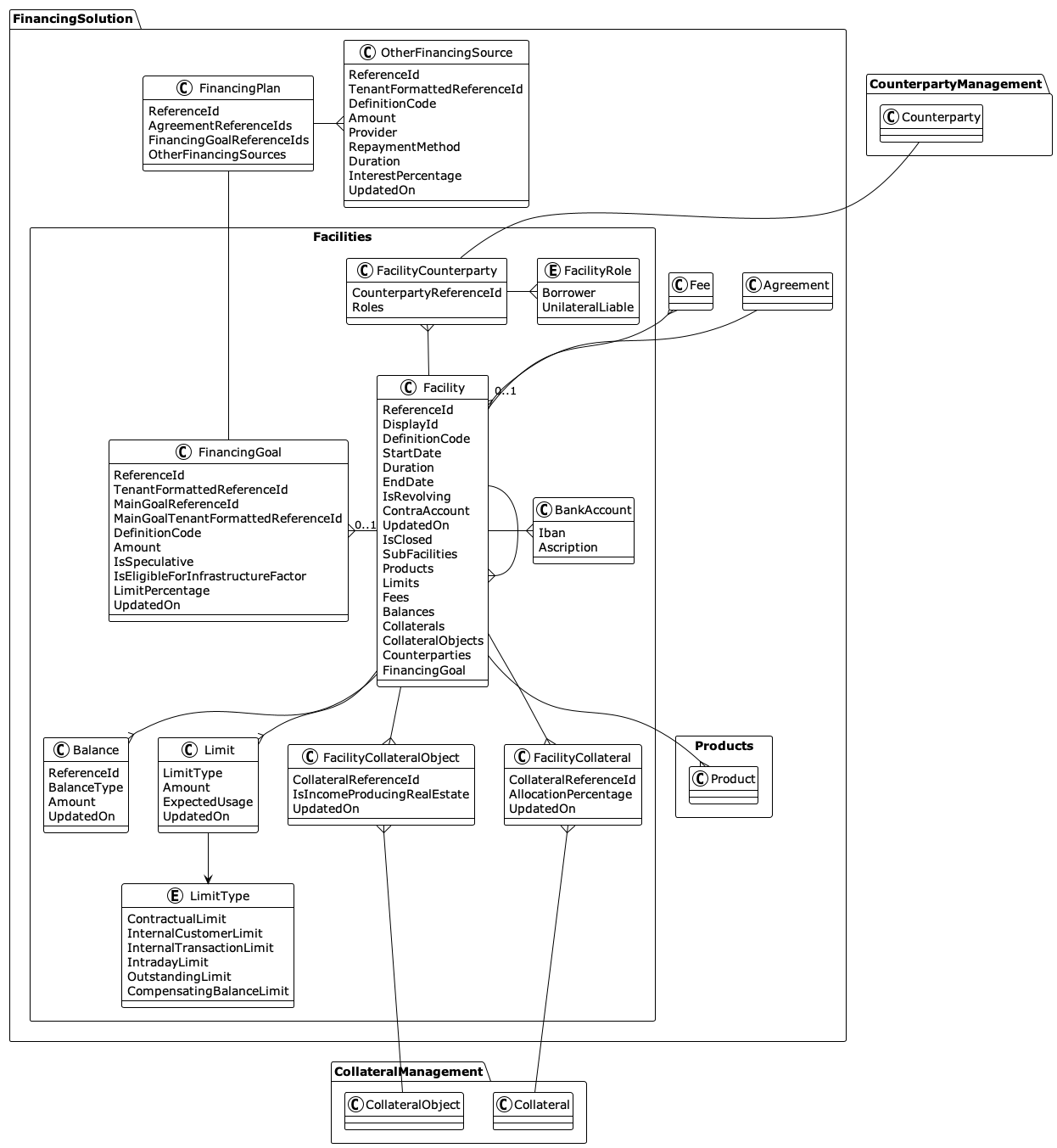

Facilities

- To view the diagram in full size, right-click and select Open Image in New Tab.

- To learn how to read the diagram, see How to read these diagrams.

A facility is a defined portion of a loan or credit line that is granted to a borrower as part of a loan agreement. It includes the amount limit, balance, duration, financing goal, and associated financial products. Each facility is typically secured by collateral or collateral objects.

In Akkuro Lending, facilities are categorized as main facilities and sub-facilities.

The main facility is defined under a loan agreement. It represents the primary loan or credit line granted to the borrower and specifies the total approved amount that can be accessed. For example, a lender may approve a $10 million loan facility for a real estate project under an agreement. This amount is the main facility.

The main facility can be divided into multiple sub-facilities, also known as loan parts. Each sub-facility is a smaller, specific portion of the main facility allocated for a specific purpose. Sub-facilities may have different terms, interest rates, or repayment schedules. For example, a main facility can be divided into 3 sub-facilities with different purposes:

- Sub-facility 1: $4 million for land acquisition

- Sub-facility 2: $3 million for construction costs

- Sub-facility 3: $3 million for marketing and operations

The main facility also includes a construction deposit as a sub-facility with a specific purpose. A construction deposit is a separate, blocked account where part of the loan facility is held specifically for new construction or renovation projects. To access the funds, the borrower needs to submit declaration invoices, such as invoices for materials or labor, as the project progresses. Once the declaration is approved, the lender releases the corresponding amount to pay those invoices. The borrower only pays interest on the amount that has been disbursed, not the total deposit. The funds must be used within a defined time period.

For example, a main facility includes a $100,000 construction deposit. The borrower submits a declaration invoice for $25,000 in materials. Once approved, the lender releases $25,000 from the deposit account to pay the invoice. Interest is charged only on the $25,000 disbursed, not the full $100,000.

To retrieve facility records, use one of the following APIs:

- Facilities Operational Query API to retrieve operational data.

- Facilities Master Query API to retrieve master data records.

Limits

Limits are the maximum amount that a borrower can borrow or draw under a facility.

To retrieve a limit record of a facility, use one of the following APIs:

- Limits Operational Query API to retrieve operational data.

- Limits Master Query API to retrieve master data records.

Balances

Balances are used only for construction deposits. They represent the remaining amount of money (AvailableBalance) left in the deposit.

To retrieve balances that are connected to a facility, use one of the following APIs:

- Balances Operational API to retrieve operational data.

- Balances Master API to retrieve master data records.

Financing goals

Financing goals describe the purpose of the facility, indicating how the borrower intends to use the loans. For example, a borrower may use a loan to purchase a house.

To retrieve financing goals that are connected to a facility, use one of the following APIs:

- Financing Goals Operational API to retrieve operational data.

- Financing Goals Master API to retrieve master data records.

Products

- To view the diagram in full size, right-click and select Open Image in New Tab.

- To learn how to read the diagram, see How to read these diagrams.

In a loan agreement, a product refers to the specific loan type offered within a facility. It combines withdrawal, repayment, and interest methods that determine how funds are disbursed, repaid, and how interest is calculated. Each facility is associated with one product to manage different aspects of the loan.

To retrieve product records, use one of the following APIs:

- Products Operational Query API to retrieve operational data.

- Products Master Query API to retrieve master data records.

Withdrawals

Withdrawals specify how the loan funds are disbursed to the borrower. It can follow one of the following strategies:

| Strategy | Description |

|---|---|

None | No withdrawal strategy applies. |

Single | The funds are disbursed once only. After the disbursement, no further withdrawals are allowed. |

Delayed | The funds are disbursed only after certain predefined conditions are met, such as collateral registration, document approval, or project milestone completion. |

Revolving | The borrower can draw, repay, and redraw funds multiple times within the approved credit limit. |

FixedTerms | Withdrawals follow a fixed schedule defined in the loan agreement. |

ConditionalSchedule | Withdrawals are scheduled but depend on specific conditions. |

IrregularSchedule | Withdrawals occur at irregular or unscheduled intervals based on the borrower’s requests or project needs. |

Declarations | Withdrawals are based on declarations submitted by the borrower or a third party, which must be reviewed and approved by the bank. |

To retrieve withdrawal records, use one of the following APIs:

- Withdrawals Operational Query API to retrieve operational data.

- Withdrawals Master Query API to retrieve master data records.

Declarations

Some withdrawals may be based on declarations. The borrowers or a third party can submit a declaration invoice to indicate the amount they need to be disbursed. This invoice can originate from either the borrower, a supplier, or a notary. Once the invoice is reviewed and approved, the system generates a disbursement to pay the amount specified in the invoice.

To retrieve declaration records, use one of the following APIs:

- Declarations Operational Query API to retrieve operational data.

- Declarations Master Query API to retrieve master data records.

To retrieve invoices connected to a declaration or by its reference ID, use one of the following APIs:

- Invoices Operational Query API to retrieve operational data.

- Invoices Master Query API to retrieve master data records.

Repayments

Repayments define how the borrower repays the loan. It includes the following repayment strategies:

| Strategy | Description |

|---|---|

None | No repayment strategy applies. |

InterestOnly | The borrower pays only the interest during the loan term, while the principal remains unchanged. The full principal amount is repaid at the end of the term. |

Linear | The borrower repays a fixed and equal amount of loan principal in each repayment. As the total amount decreases over time with each repayment, the interest also decreases. |

Annuity | The borrower pays a fixed installment, including both interest and principal in each repayment. Over time, the interest portion decreases and the principal portion increases, keeping the total payment constant. |

Revolving | The borrower can draw, repay, and redraw funds up to an approved credit limit. Repayments restore the available credit, and interest is charged only on the utilized amount. |

IrregularSchedule | The repayment schedule does not follow a fixed pattern or frequency. Payments may occur on irregular dates or in varying amounts, often based on specific contractual agreements or exceptional cases. |

To retrieve a record of repayments, use one of the following APIs:

- Repayments Operational Query API to retrieve operational data.

- Repayments Master Query API to retrieve master data records.

Interest products

Interest products define how interest is calculated, structured, and applied to the loan over time. It includes the rules, rates, and components that determine the cost of borrowing. A product may have zero or more interest compositions.